The Epic Retirement Tick –

powered by Chant West

We've developed a benchmark that will help you spot the super funds that support your best retirement. It's called The Epic Retirement Tick and it's powered by leading research house, Chant West.

Sign up to receive the report (free)The Epic Retirement Tick is here to make life simpler for Australians heading into retirement.

The Epic Retirement Tick is here to help you see, at a glance, which super funds are truly set up to support you in the most important years of all—your Prime Time and your retirement.

Developed by the Epic Retirement Institute in partnership with leading research house Chant West, the Tick is awarded to funds that meet a clear set of criteria showing strong support for members in the lead-up to and throughout retirement.

Unlike the government’s performance test, which focuses only on investment returns and fees, the Epic Retirement Tick looks at the whole picture. It checks whether your fund offers the right mix of investments, income products, advice, education, tools, and service standards that can make a real difference when you’re approaching or living in retirement.

It’s not a rating, award, or personal recommendation. It’s a clear, fact-based way to see whether a fund meets a high benchmark across 18 key areas that matter most in retirement.

What getting the Epic Retirement Tick means

When you see the Tick on a fund's website, marketing or tools, you can be confident the fund has met the high standards of this assessment. To qualify, a fund must perform strongly in most of the measures across at least 12 of the 18 key categories.

That means the fund offers a broad, practical range of services designed to support members both before and during retirement. It doesn’t guarantee it’s the best fit for you—your personal needs, goals, and circumstances will always matter most—but it does show the fund is delivering well in many of the areas that count at this stage of life.

What the Tick is not

The Epic Retirement Tick is not:

- A “best fund” list

- A product recommendation

- Personal financial advice

Sign up to receive the report

Sign up now to receive the free Epic Retirement Tick Report direct to your inbox when it’s released on 2 October 2025.

Be the first to know which funds have earned the Epic Retirement Tick, and learn about how you can apply the criteria to your fund.

Why it matters

Most people have no idea what their super fund should be doing for them in the run up to retirement and in retirement. That is why we built this framework, to encourage transparency and higher standards across the industry.

When more Australians can see clearly what “good” looks like, more funds will work to deliver it. That means better retirement outcomes for everyone.

The Epic Retirement Tick is more than a benchmark. It is a tool you can use in the run up to retirement and in retirement to decide whether your fund is good enough - and a consistent framework we can all use to push the superannuation industry to do better.

When members know the standard and start asking their funds tougher questions, funds pay attention. And when enough of us ask in an organised way, change happens.

By understanding the 18 key criteria and checking whether your fund has the Tick, and asking them if they don't - why they aren't as focussed on retirement, you are helping to create the peer pressure that drives real improvement.

Together, we can lift the bar so more Australians get the retirement support they deserve from their super funds—and take action to move if they don’t.

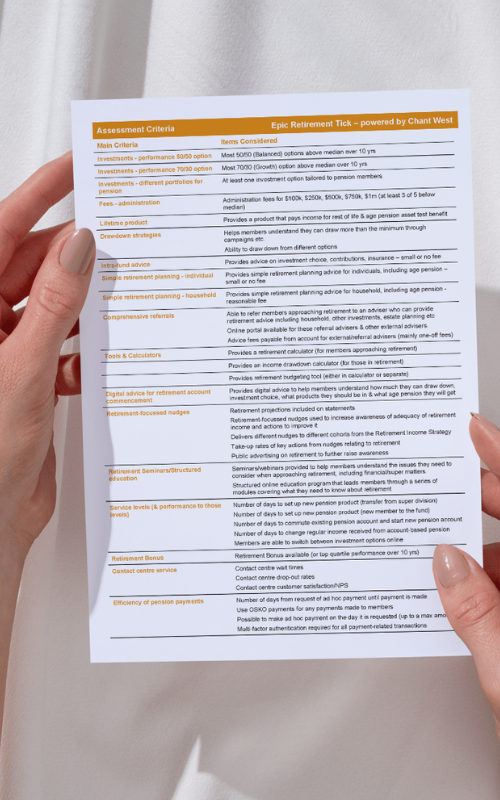

The 18 key criteria

The Chant West team is assessing funds against 18 well-considered criteria. Which of these matter most to you is a personal choice, because different funds serve different types of members, and what’s important for one person may not be for another.

1. Balanced investment performance above the median over 10 years

When you are looking at a fund’s balanced (50/50) option, long-term consistency of their balanced investment option really matters. This is not about chasing last year’s hot result or marketing you their highest recent performance. The benchmark here is strong, steady returns over 10 years compared with other funds. It shows your fund can manage a mix of growth and defensive assets well over time.

2. Growth investment performance above the median over 10 years

If you have a longer horizon or are comfortable with more ups and downs, a growth (70/30) investment option can give your retirement savings more room to grow. This criterion checks whether your fund’s growth option has beaten the median over 10 years. Sustained outperformance in this higher-growth mix is harder to achieve.

3. Tailored pension portfolios

Once you start drawing an income from super, your investment needs change. A fund should offer an option built specifically for pension members. The aim is to balance income needs with capital protection and tax efficiency. The decumulation phase is different from the growth phase.

4. Low admin fees

Fees do not stop being important once you are in retirement. Every dollar in fees is a dollar you cannot spend on your life and a dollar that doesn't compound. This standard looks at admin fees across multiple account sizes. We review account balances of $100k, $250K, $500k, $750k and $1M and expect at least 3 of the 5 options to have fees below the median. A fund with a tick in this assessment criteria should be shown to offer competitive fees no matter your balance.

5. Lifetime income products

For many Australians, the fear of outliving their money is real. Funds that tick this box offer an income-for-life product for their members. Often, these products are treated favourably under the Age Pension assets test which can help you boost your overall income.

6. Flexible drawdown strategies

The minimum drawdown set by the government for people in the retirement phase of superannuation is just that, a minimum. Sometimes you might want or need to take more and evidence shows that many can afford to spend more during some phases of their retirement. A good fund helps you understand the impact of different drawdown levels and additionally, they give you the flexibility to pull income from different investment options within your account so you aren’t forced to sell from your growth assets if they’re underperforming at a point in time.

7. Intra-fund advice

You should not have to pay thousands of dollars for help with the basics of using your superfund well to grow your money. Superfunds should provide good intra-fund advice. Intra-fund advice covers things like assessing your risk appetite, choosing your investment option, deciding how much to contribute to your fund, or checking your insurance is still right for you. This is usually provided for little or no cost and is an important service for people starting to think more about their super.

8. Simple individual retirement planning

When you are five to ten years out from retirement, your questions change. This is where simple, low or no-cost financial planning to support your journey into retirement comes in, including working out if you might qualify for the Age Pension, and what that would mean for your income mix alongside your super. Funds will be assessed against their ability to provide this for a small fee or no fee.

9. Simple household retirement planning

Retirement planning often is not a solo sport. This is about affordable advice that looks at the whole household. It considers your partner’s super, investments, income streams, and any Age Pension entitlements so you can plan together. We will review funds services to assess whether they are able to help you for a small fee or no fee.

10. Comprehensive advice referrals

Sometimes you need the whole financial picture - and for this you might need comprehensive financial advice. This type of advice includes your super, other investments, estate planning, and even aged care considerations. Funds that meet this criterion can refer you to a trusted adviser either inside or outside their business. We will also assess whether they allow you to pay for the advice from your super account, especially for one-off plans. And, look at whether they have an online portal available for external and referral advisers to streamline interactions.

11. Retirement calculators and budgeting tools

A good fund arms you with tools that take the guesswork out. Retirement calculators show you what income you can expect, drawdown calculators help you test different withdrawal rates, and budgeting tools help you plan the life you want to live, not just survive. We assess each fund for three types of calculators and to get a tick they need to have 2 of the 3:

- Retirement calculator

- Income drawdown projection calculator

- Retirement budgeting tool

12. Digital retirement advice

Think of digital retirement advice as personalised guidance without the face-to-face meeting. We’re going to see more and more of it. The best funds offer online tools that recommend a drawdown rate, help you pick an investment mix, and estimate your Age Pension based on your numbers. Some offer some impressive digital advice services. Others not so much.

13. Retirement-focused nudges

Sometimes we all need a tap on the shoulder to remind us of the things we should be doing with our super. These nudges can be retirement projections on your statement, targeted emails about boosting your contributions, or prompts to attend a seminar. The best funds tailor these nudges to your age and stage. We’ll be assessing funds against a few different types of nudges:

- Whether they deliver different nudges to different people based on where they are in life.

- Whether their nudges actually work (via assessment of their take up rates)

- Public advertising on retirement to further raise awareness - because it’s a poorly understood phase of superannuation

14. Retirement education programs

Not everyone learns by reading a fact sheet or crawling through a website trying to find what they need. Some funds run retirement webinars, in-person seminars, or structured online courses that walk you through the key steps to get retirement-ready. They make these easy to access and understand. So we’ll be assessing funds on two types of education:

- Whether they provide seminars and webinars to help people understand the issues they need to consider when approaching retirement

- And whether they provide structured online education programs to help people learn in an organised manner.

15. Service levels

When you open a retirement account with your super fund, or make a change to your pension account, you should not be waiting weeks. This measure looks at how quickly a fund can set up, switch, or adjust your account and whether you can do it online. We assess funds by:

- The number of days it takes to set up new retirement/pension accounts,

- Commute an existing pension and start a new pension account; change the regular income received from their super fund

- And whether members can switch between investment options online

16. Retirement bonuses or top performance

Some funds offer a retirement bonus when you switch from the accumulation phase into the retirement phase of super, essentially giving back the tax that was provisioned for them, to the members. We assess whether funds offer this.

We also bear in mind that a fund that has top-quartile investment performance may actually be delivering more over the long term than a retirement bonus would.

Either way, it is a sign your fund is finding ways to give you more value.

17. Contact centre service

When you have a question for your superfund, you want a quick, clear answer from someone who knows their stuff. This criterion looks at wait times, call drop-outs, and customer satisfaction scores of their content centre. In retirement, good service is quite frankly not optional.

18. Efficiency of pension payments

Need an ad hoc drawdown from your superfund? The best funds can do it fast, sometimes the same day, and securely. So we’re assessing which ones can. We’ll be checking:

- The number of days a fund takes to pay you, from the request of payment until the payment is made

- Whether they use OSKO payments, Australia’s near-instant bank payment system run by BPAY to make payments fast and efficiently

- Whether they offer same-day adhoc payments (up to a max amount)

- And whether they offer multi-factor authentication to protect you from fraud.

Key dates for the Epic Retirement Tick

We are rolling out the Epic Retirement Tick in stages so Australians can first understand the criteria and classification process, then see which funds have earned the tick. Here is what to expect:

20 July 2025

Criteria sent to all super funds for assessment. We have invited funds to submit the data required to do the assessment.

16 August 2025

Public announcement of the Epic Retirement Tick and the 18 key criteria we believe consumers can choose to assess their own super funds by.

2 October 2025

Release of the first annual Epic Retirement Tick Report and list of funds that achieved the Tick.

From December 2025

Ongoing updates, insights, and annual reassessments.

If you are with a fund that has earned the Tick, you will start seeing it in their member communications from October 2025. If you are not, it might be time to ask your fund what they are doing to prepare you for retirement and where they could do better. Together, we can drive funds to do better.

About the partnership

The Epic Retirement Tick was co-developed by Bec Wilson, founder of the Epic Retirement Institute and author of How to Have an Epic Retirement and Prime Time: 27 Lessons for the New Midlife, and Ian Fryer, General Manager of Chant West.

Bec brings a focus on empowering everyday Australians with clear, practical education about midlife and retirement. Chant West brings decades of superannuation research and ratings and a mission to build a better retirement system. Together, we have created a benchmark that rewards strong retirement support and pushes the industry forward.

Where else can you learn about the Tick?

You can explore more about the Epic Retirement Tick in Prime Time: 27 Lessons for the New Midlife and the upcoming December 2025 release of How to Have an Epic Retirement. It’s also regularly featured in the Epic Retirement newsletter, on the Prime Time podcast, and in ongoing media conversations.

The Tick gives us a clear framework for defining what ‘good’ looks like for everyday people who use super—so conversations can lead to real action from both consumers and funds, rather than just adding to the noise about what’s wrong with super and retirement.

Explore Prime Time

Frequently Asked Questions

What is the Epic Retirement Tick?

Does the Tick mean a fund is the best in the country?

Does the Tick mean I should switch funds?

How can I use the Tick to check my fund?

Where can I find the list of funds with the Tick?

What if my fund doesn’t have the Tick?

Can a fund be reassessed before the next annual report?

Why do we allow mid-year reassessments?

What happens when a fund earns the Tick mid-year?

Sign up to receive the report

Sign up now to receive the free Epic Retirement Tick Report direct to your inbox when it’s released on 2 October 2025.

Be the first to know which funds have earned the Epic Retirement Tick.